Chicago Fed: Midwest ag land

values increased in first of ’18

By DOUG SCHMITZ

Iowa Correspondent

CHICAGO, Ill. — The Federal Reserve Bank of Chicago has reported

Midwest farmland values have increased in the first quarter of this year, showing

signs of stabilizing and remaining unchanged from a year ago.

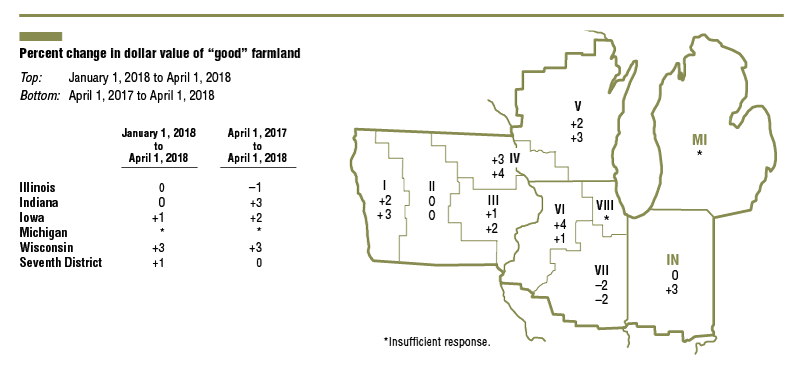

That’s according to recent survey responses of 181 agricultural

bankers from the Seventh Federal Reserve District, which includes Illinois,

Indiana, Iowa, Michigan and Wisconsin.

“On average, ‘good’ farmland values in the first quarter of 2018

rose 1 percent from the fourth quarter of 2017,” said David Oppedahl, Chicago

Fed senior business economist, who conducts the district’s quarterly surveys.

This increase in district ag land values marked the fifth quarter

in a row without a decline in such values. “Illinois and Michigan (the latter

based on a handful of responses) were the only district states to experience

year-over-year decreases in farmland values,” he explained.

While farmland markets saw supply rising a bit, demand and sales

slipped, he added. “There was an increase in the amount of agricultural land

for sale during the most recent winter and early spring relative to a year ago,

as 27 percent of the responding bankers reported more farmland was up for sale

in their areas, and 23 percent reported less.”

With 18 percent of the survey respondents reporting higher demand

to purchase farmland and 20 percent reporting lower demand, Oppedahl said there

was almost an even split among those who perceived a shift in interest on the

part of buyers in the three- to six-month period ending with March 2018,

relative to the same period ending March 2017.

In addition, with cash rentals making up 80 percent of district

agricultural land operated by someone other than the owner, changes in their

terms are a key indicator of agricultural conditions, he said.

“Cash rental rates for farmland in the district decreased 5

percent for 2018 relative to 2017 – the smallest decline in four years.” In

fact, for 2018, average annual cash rents to lease farmland were down 5 percent

in Illinois, 3 percent in Indiana, 6 percent in Iowa, 3 percent in Michigan and

7 percent in Wisconsin, he said.

“There seemed to be enough farmers willing to take on more acres

to plant, such that cash rents did not fall as much as they would have

otherwise,” he said. “Meanwhile, other farmers quietly ended their rental

contracts, even defaulting on payments to landowners, in some cases.”

Released May 15, the survey results also showed 2018’s real cash

rental rates were 26 percent below their level in 1981, while real farmland

values were still 67 percent above their 1981 level.

“Hence, the implication is that relatively stronger demand to own

farmland than to lease it has kept farmland values from falling as much as the

earnings potential of farmland (represented by cash rental rates),” Oppedahl reported.

In March 2018, he said corn and soybean prices were about the

same as a year ago, according to data from the USDA; however, the five-year

drops in real corn and soybean prices were 54 and 37 percent, respectively.

“Since these price decreases would have resulted in greater

declines in crop revenues than observed in cash rents over the past five years

(all else being equal), farm operations needed productivity gains through

higher yields and cost-cutting measures in order to preserve working capital

and maximize cash flows,” he said.

In addition, district agricultural credit conditions tightened

further during the first quarter of 2018.

“Once more, repayment rates for non-real estate farm loans were

down from a year ago, and renewals and extensions of these loans were up from a

year earlier,” he said. “Demand for non-real estate loans in the first quarter

of 2018 was higher than a year ago, while the availability of funds to lend was

somewhat lower.”

Chris Hurt, Purdue University professor of agricultural

economics, noted that Midwest land values adjusted downward in 2014, 2015 and

2016.

“In 2017 and 2018, they have exhibited more stability or

bottoming,” he said. “Generally, the amount of land available for sale has been

lower than normal as the U.S. Fed kept interest rates low.”

Hurt said families that owned farmland could earn nearly 3

percent from cash rent and CDs had lower returns than cash rent, adding that CDs

are a common alternative way to invest capital for farm families.

“Times are changing,” he said. “Global weather has been less than

ideal in 2018. Dropping production and world economic growth is supporting

strong usage. As a result, excess grain stocks are declining and farm prices

are improving. Inflation is likely to continue to pick up, and this will

initially support farmland values.”

Hurt said farmland buyers also generally believe that in the

longer run, basic food production will be a favorable industry.

“The current outlook for operating margins on Midwest grain farms

are expected to improve in 2018 and again in 2019, suggesting an upward

trajectory for the grain-farm economy in recovery from extreme lows,” he said.

“Operating margins in 2018 are still negative, which means they

will not cover all of the overhead costs associated with machinery ownership

and providing a reasonable labor return, but they are improved from the past

four years.”

Moreover, a headwind to further increases in farmland values will

be higher costs of production and higher interest rates. “Higher costs are

almost universal in 2018: machinery, fertilizer, fuel, chemicals, labor and

interest rates. The 10-year Treasury yield has now pushed higher than the 3 percent

cash rent return,” he said, “and may provide incentives for some additional

families to sell farmland.

“In addition, a 3 percent, 10-year Treasury yield is consistent

with a real estate loan rate at commercial banks in the Chicago Fed district of

about 5.5 percent, the highest level since 2011. Higher interest rates will

encourage more farmland sellers and discourage some buyers.”

|